Disclaimer: This is just a running diary where I consolidate my portfolio status on a monthly level, usually at the end of the month. This is in NO WAY an Investment Advice and is not intended to be a recommendation. Please check with a SEBI registered financial adviser for legal advice before investing.

In my last post, I had reviewed our current performance. Of course, I didn’t share much details about the stocks and MF portfolio. I guess the readers of the blog (if they exist :)) seem not to care. In any case, one of my friends recently remarked, “Dude.. It’s been a while since you updated the blog”. Well, this is the spark I required and lo! behold.. I am now updating the blog with my latest portfolio.

Some recent emergencies meant I had to remove some funds from my stocks portfolio. Once the emergencies tied over, I have reinvested most of the money back. However, over the past couple of months, I have been redefining the way I want my portfolio to look. There are a lot of discussions that me and another friend of mine have on these topics and together, we are trying to find an optimal way .. i.e. if it exists. Along the way, we can also feel that our skills are also getting updated.

Some generic changes include:

- Book Profits when the original investment rationale doesn’t hold good (see below)

- Weed out non-performers as early as possible

- Build a concentrated portfolio

The past month has been filled with a few of firsts for me as I will try to capture below.I am still debating about Core and Satellite approach, but more on that later. However, it’s been a learning and humbling experience which I hope will stand me in good stead going forward.

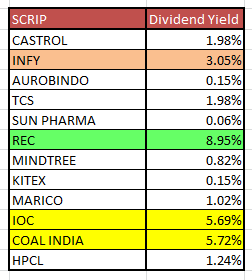

Stocks – Self

Changes:

- Exited Infosys and TCS – Reinvested the same across other stocks

- Concentrated the portfolio by reducing the no. of stocks from 19 to around 12

- Added some new counters – Apcotex, Arman Financial, Divis

- Booked 50% loss in Nitin Fire Protection Services – Lesson learnt – Never leave one word out from the literature

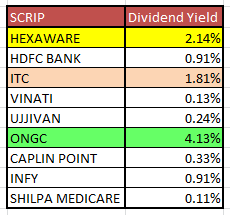

Stocks – Better half

Changes:

- Exited the first Multi-bagger Vinati Organics as the original investment rationale didn’t hold good

- Will watch Vinati and re-enter if the valuations become attractive again

- Redistributed the gains and original investment across other stocks

MF Portfolios

In the recent few months, I have invested in some closed ended funds which are giving some pretty good returns. I have also stopped some of the manual SIPs and redirecting the money into stocks.

Money is in the market, albeit not in MF, but direct stocks.

Suggestions / Comments / Feedback most welcome.